Facing a Mortgage Crisis? What to Do When Payments Suddenly Slip Out of Reach

The majority of individuals don’t anticipate that they won’t be able to make their next mortgage payment when they wake up one morning, yet it does happen more frequently than you might imagine.

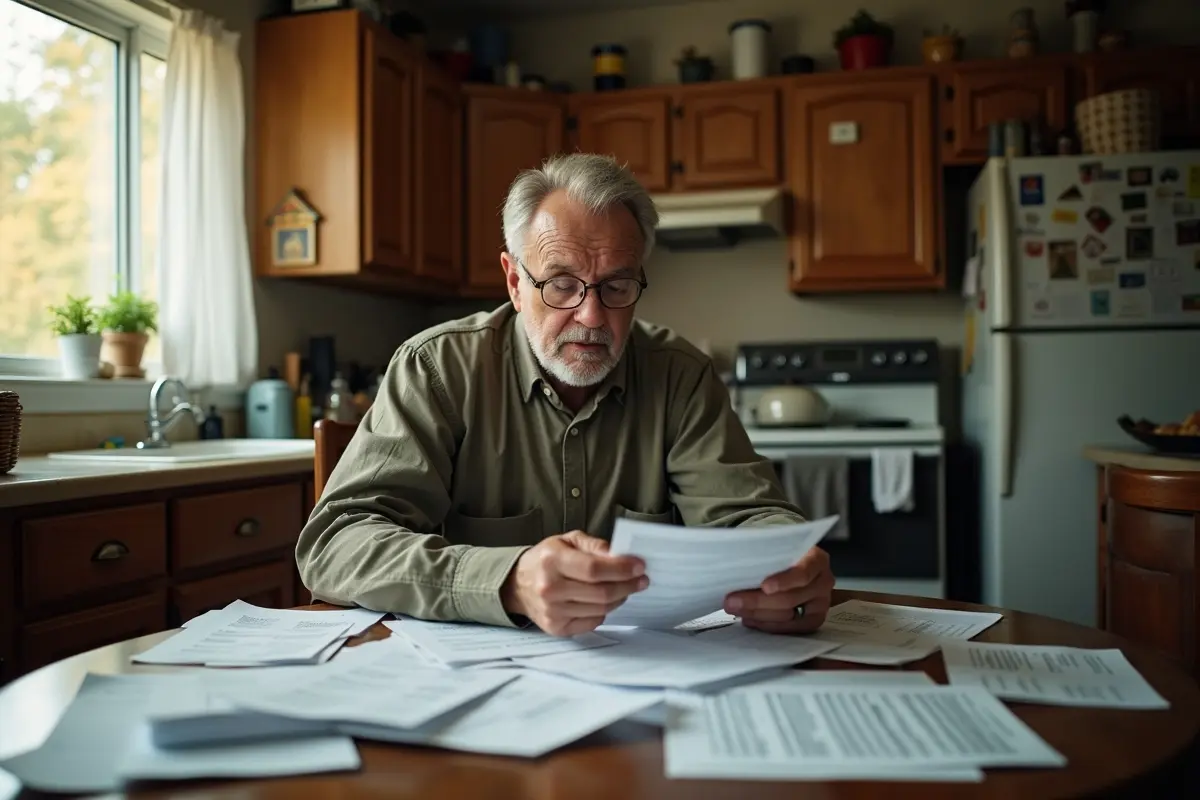

A medical emergency, unplanned repairs, job loss, or any other type of financial emergency can completely disrupt your budget. The issue is not the setback as such, but rather how easily people become overwhelmed and uncertain of their options. In actuality, you probably don’t know how many options and rights you have.

Contents

Face The Facts

Knowing that silence is your enemy is the first step when finances are tight. Many homeowners wait to “figure it out next month” or avoid answering their lender’s correspondence. By then, the issue has gotten worse, and late fees have accumulated.

Instead, get in touch with your loan servicer as soon as possible. Most lenders would like to assist you in getting back on track rather than proceed with foreclosure, even though it could be uncomfortable. You might be eligible for hardship forbearance, short-term payment reductions, or changes to your repayment schedule. You have to initiate the conversation in order for any of these possibilities to show up.

Explore Your Short-Term Finances

Examining your short-term financial situation honestly is also crucial. When negotiating with your lender, it will be helpful to carefully document any temporary issues, such as a brief period of unemployment or an unexpected medical expenditure.

You’ll need a different strategy that safeguards both your house and your future financial security if the issue appears to be more persistent.

Reach Out to Expert Lawyers

At this point, expert advice becomes crucial. Many homeowners mistakenly believe that foreclosure is an easy procedure that they have little control over.

Early communication with foreclosure lawyers frequently results in a very different outcome. These lawyers are aware of the deadlines, notices, legal rights, and procedural obligations that homeowners may not be aware of. They may advise you on how to prevent needless anxiety as well as what your lender can and cannot do.

More significantly, a lawyer can assist you in determining if the servicing of your mortgage was appropriate. Most people are unaware of how frequently mistakes are made in loan modification processes, misapplied payments, incorrect notices, or infractions of federal mortgage servicing regulations. Without expert assistance, these subtleties are typically overlooked until it is too late to address them.

Consider Selling or Refinancing

If debt restructuring is insufficient, you might think about selling or refinancing before things get worse. Selling on your own terms is vastly preferable to losing your house through a court-driven procedure, even though it may seem like an emotional choice. You may protect your equity and get the breathing room you need with a well-thought-out sell.

The most crucial thing to keep in mind is that a mortgage setback does not equate to personal failure. Even financially savvy homeowners occasionally face challenges due to life’s unexpected turns. It depends on who you ask for assistance from and how fast you act.

You can safeguard your rights and save a difficult situation from developing into an extended crisis by acting quickly, getting legal advice, and looking into all of your options.